Putting a stop payment on a misplaced or stale check may prevent issues down the road, especially if there’s a concern that it could fall into the wrong hands. However, this doesn’t always solve the problem, as it costs a fee to the payor and is only valid for a limited time. The payee will find the money didn’t arrive in their account, which could, in turn, even cause them to overdraft their own account.

What are Late Payment Penalties?

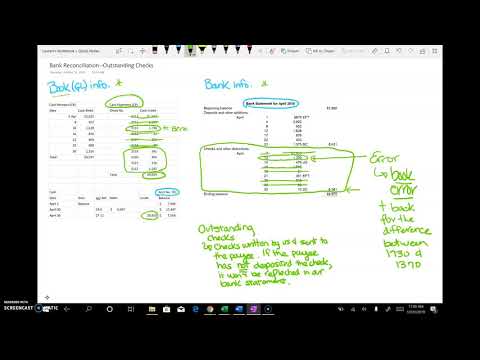

By tracking outstanding checks, businesses can ensure the check status outstanding meaning integrity of their financial reporting, manage cash flow effectively, and prevent discrepancies that can impact their financial stability. It is essential to understand the causes of outstanding checks, the consequences of not managing them, and the methods to identify and reconcile them. Reconciling outstanding checks involves verifying deposits, investigating discrepancies, and updating the check register accordingly. Regular reconciliation ensures accuracy in financial reporting and helps prevent potential cash flow issues. In summary, tracking outstanding checks is vital for businesses to maintain accurate financial records, manage cash flow effectively, and prevent discrepancies. By diligently monitoring and reconciling outstanding checks, companies can make informed financial decisions and ensure their financial stability and success.

How Can You Determine A Company’s Net Working Capital From A Balance Sheet?

By not trusting the payee to take action, you remove the possibility that they will forget or put off cashing or depositing the check. Outstanding checks may cause issues for both the payor and the payee. On the payor side, it creates the need https://ladecoupe76.com/understanding-notes-payable-journal-entries/ to carefully track uncashed checks so that money doesn’t get spent on other things.

How Much Money Is 6 Digits? Income vs. Net Worth

The payor has no control over when the payee will cash or deposit the check. The only thing the payor can do, for a fee, is stop payment on the check. The payee cannot cash or deposit the check once a stop payment has been issued.The payer’s bank has no way of knowing that a check has been written until the payee deposits or cashes the check. Besides the liability it creates, the payor may forget that they wrote the check and spend money allocated for the check. When the payee cashes the check, and their bank tries to pull funds from the payor’s account, the payor will get hit with an overdraft or non-sufficient funds (NSF) fee. The payor can void these fees using overdraft protection on their checking account.

For example, if you made $1,000 in purchases during a billing cycle and your balance was $0 before that, your next statement balance would show an amount of $1,000. Online payments offer a more direct way of transferring the funds between you and the payee. As a result, your available balance may not reflect the actual spendable cash, leading to a misinterpretation of your financial standing.

- Imagine sending out payments as smoothly as pouring water into a glass.

- For instance, a 2-for-1 stock split reduces the price of the stock by 50%, but also increases the number of shares outstanding by 2x.

- Imagine a scenario where Sarah, a small business owner, writes a check for $800 to pay for monthly rent on her office space.

- Explore the financial implications of outstanding checks, including their effects on account balances and reconciliation processes.

- The receivable balance is the total outstanding amount of revenue that you have billed to customers but not yet collected.

Your available credit is usually your credit limit minus your outstanding balance and any pending transactions. As someone who works in IT, I can explain why this happens from a technical perspective. EDD likely uses multiple databases that sync on different schedules – one for payment processing and another for the UI display system. When you certify and get paid quickly, the payment database updates first (hence money in your account), but the UI display database might only sync every few hours or overnight. This is actually pretty standard for large government systems that prioritize getting payments out over real-time status updates.

- Most banks will continue to honor checks for the full 180 days, but that isn’t guaranteed.

- What happens if I write a check but the payee doesn’t cash it right away?

- Additionally, banks may have policies regarding check validity periods and fees for processing stale checks.

- Also, outstanding checks may prove a hassle for an otherwise careful consumer.

Alternatively, if you both use the same bank or credit union, the transaction will conclude when the money is transferred from your account into the payee’s account. Once such checks are finally deposited, they can cause accounting problems. Furthermore, checks that are never cashed may constitute “unclaimed property” that is turned over to the state. Checks which have been written, but have not yet cleared the bank on which they were drawn. In the bank reconciliation, outstanding checks are deducted from the balance per bank.

The Risk of Stale Checks and the Need for Stop Payments

Disputes may arise if a payee claims non-receipt or loss of the check, requiring the issuer to issue a replacement, which increases administrative burdens and the risk of duplicate payments. For businesses and individuals alike, outstanding checks can introduce uncertainty into cash flow management. These checks represent funds subtracted on paper but not physically withdrawn. If want to avoid Outstanding Checks altogether, consider online bill payment. With this, the bank deducts funds from your checking account when the check is printed.

- The ‘outstanding’ status is just a lag in their system updating – nothing to worry about.

- If a check remains outstanding for an extended period, consider contacting the payee to remind them about the pending transaction.

- Outstanding personal checks can cause budgeting problems, but you may have an easier time reminding a friend or family member to cash a check than a business payee.

- This approach helps to keep issues with the check in check and work toward rectifying them before they become challenges.

- You can also consider digital money transfers to avoid the issue of paper checks entirely.

- During this time, the outstanding check is still liable for the issuer’s account balance.

If you’ve received an outstanding check, deposit or cash it promptly. After investigating the cause of an outstanding payment, specific actions can Bookkeeping for Chiropractors resolve the situation. If your investigation reveals that the payment was not yet sent, immediately initiate it through appropriate channels, such as online banking, a vendor portal, or by mail. Ensure all payment details, including the amount and recipient information, are accurate to avoid further delays. Have you ever experienced the frustration of receiving an outstanding check due to insufficient funds? It can be quite a headache, especially when you were counting on that money.